Recap: Nintendo Inc

Materialization of Nintendo Thesis

Dear Readers,

I hope you are well. The past month has kept me occupied with work and exams, but now that they're behind me, I can redirect my focus to what I'm most passionate about - contemplating businesses. In today's brief article, I'll share how my perspective on Nintendo (TSE: 7974) has evolved over the past year and my renewed thoughts on the company. While this piece may be concise, I hope you can still extract some key insights.

I assume that most of you are acquainted with the video game company, Nintendo. For those who might not be, here's a succinct definition of what Nintendo is, or at least, has been historically.

Nintendo Inc is a Japanese, vertically integrated video game developer with a broad portfolio of “AAA” rated intellectual properties, including Super Mario, Legend of Zelda, and Pokémon. Gamers can indulge in these latest experiences by purchasing Nintendo’s walled-garden platform, the Nintendo Switch.

I first bought into Nintendo in early April 2023, when I first wrote about my 20-page paper on Nintendo, explaining why it is as an undervalued, high-quality, and sustainable growth company. Back then, I received comments that Nintendo should not be classified as a value stock as its share price is at its “all-time-highs” but truth be told, I never understood that rationale.

I will not bore you with the intricacies of the financials, though I highly encouraged you to spend some time and look at the amazing story that is unfolding, but generally, there are 3 key ideas in my thesis paper.

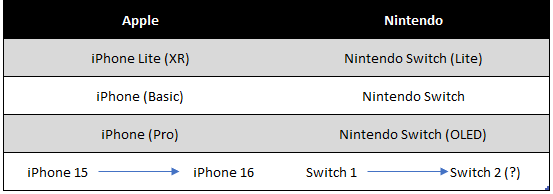

Nintendo’s cyclicality as a video-game platform developer and its dependence on hardware sales are diminishing. This decline is propelled by a shift in the business model: one that strives to establish a consistent flow of recurring revenues through its online subscription offering (Nintendo Switch Online) and an adoption of Apple’s iterative product playbook for its platforms (though it has yet to be proven). Why is this good? Because investors do not like uncertainty. Following a iterative model with obvious upgrades seems like a high conviction strategy that investors can get along with. To me personally, it matters because of the fact that Nintendo would not need to rebuild its user base. This, to me, is the most important factor.

Nintendo’s management has finally started taking steps to actively monetize its valuable IP such as in movies and more interestingly, in theme parks through a partnership with Universal Studios. These asset-light, high return on invested capital projects are signs of wise capital allocation and, in my opinion, inspired my view on the “Flywheel effect” that Nintendo is executing on. These aren’t just efforts to diversify revenue streams; these are strategies that will enhance Nintendo’s core business - selling games and platforms. This is why it is so amazing that the Switch, in its 7th year, just experienced one of its best quarters since release. I guess shareholders all have to thank Chris Pratt’s wonderful performance.

A point that I would like to make is that fundamentally, these projects are not there to just promote Nintendo’s characters which in turn, drive console and software sales. While it is indeed true that we will see the results of the Flywheel relationship through these quantitative metrics, what Nintendo is essentially just trying to do is to 1. Increase exposure and awareness of Nintendo brand to new and current audiences and 2. Promote the “goody-vibes” that is associated with the Nintendo brand. Just like how Coca-cola stands for happiness, Nintendo is trying to associate the cozy feeling of gaming together in an intimate setting, just like how one used to do when he or she was young.

Why is this important? This is important because of the fact that in the video-games and entertainment industry at large, the strength of your intellectual property is the key indicator of pricing power. Put it simply, is someone more inclined to buy a Marvel title “Iron Man - Defenders of Earth” video game for $69.99 or “Legend of Zelda- Tears of the Kingdom”. This brand strength is one that will allow the business to leverage more revenue derivation in manners that one can yet to see now.

Lastly, gaming penetration as a whole is increasing. The time spent on gaming is drastically different now compared to 20 years ago. With each passing year, the gaming industry, and the world in general, is replacing its non-gaming generation with a gaming-inclined generation. I personally believe that this trend is, at best, in its mid-cycle. The best is yet to come, where across age groups, we will have gamers.

I understand that this might sound a bit controversial; Gaming? When you are in your 80s? Impossible! Well, that’s because we view gaming as a "time-killing," thrill-seeking activity that youngsters use to escape from reality. While this may be partly true, video games are not just that. If we start to see how gaming has evolved, from the emphasis on individual experience (solo) to LAN and now to massively multiplayer online cooperative formats, gaming is not just a thrill-seeking activity; it is, in essence, a social activity. If social games like Bridge and Bingo continue to be fashionable among older age groups, it may not be far-fetched to see future digital alternatives picked up by an older age group conditioned and exposed to digital realities since birth.

Lastly, there is an increasing trend of improving female-gamer penetration. As an industry, the customer mix is slowly shifting from a male-dominated segment to a balanced, 50-50 mix between males and females. This trend has 2 implications for Nintendo, not only is it just better economics for the industry overall, it is specifically better for Nintendo whose title’s are generally, lower barrier of adoption for female gamers who are casual gamers or just starting out.

Other peripheral impacts includes the digitalization of software (Games) sales, which in turn improves the overall margin for Nintendo (though recent quarterlies shows that this shift towards a 70% digital sales might take longer than expected).

Nonetheless, in conclusion, what do we have? An internationally beloved company, coupled with sustainable, long-term secular drivers, supported by the best-in-class assets of character franchises and renewed enthusiasm from management to start monetizing its IP. With the new Zelda, Yoshi movies and a rumored launch of Switch 2 next year, tell me again, how can one not be excited for Nintendo’s future?

But hold on, what is the risk? Where can it all go wrong?

In all seriousness, risk is something to consider, particularly when exploring fundamental shifts in consumer preferences. For example, the same argument applies to Disney and its AAA-rated Marvel portfolio, featuring Iron Man, Spiderman, Hulk, Thor, and more. However, it's clear that after a decade of Marvel content, consumers as a whole have begun to experience brand fatigue with Marvel franchises. The same "Loki" sequel no longer excites us as much as the initial "Avengers" series did. In my opinion, brand fatigue is a key risk for Nintendo's strategy. I believe this phenomenon will accelerate more for Nintendo compared to Marvel's 10-year run. Why? I can't fully justify it now, but in short, Marvel initially had the edge of a new format, combined with an innovative "cross-over" system that was previously unseen, maintaining momentum. I believe Nintendo can do the same, perhaps with a crossover of Super Mario, Pokémon, and Zelda in a Super Smash Bros universe. However, consumers already expect this, making them less likely to be as fascinated as before. Nonetheless, I believe we are still in the early stages of this cycle and that there is still quite a distance before this happens. Furthermore, the double-edged sword of management's resistance to eroding the brand for short-term financial outperformance is one that, I believe, would further reduced the occurrence of the consumer fatigue risk.

For now, Nintendo still remains my top pick in the video-game space.

P.S. At the time of my writing, I have received news that Charlie Munger has regrettably, passed away as of this morning. My heartfelt condolences go out to Mr. Munger's family. I'll forever appreciate his teachings and, more significantly, the profound impact his life philosophy has had on me. Thank you, Mr. Munger.

Disclaimer: Not Financial Advice - Please Conduct Your Own Research

The content on this investment blog is intended for informational purposes only and should not be construed as financial advice. It does not consider your specific financial situation or objectives. All investment decisions should be made after conducting thorough research and, if necessary, consulting with a qualified financial advisor. The author and the blog are not responsible for any financial decisions made based on the information provided. The financial landscape is subject to change, and readers are encouraged to verify information independently, recognizing the inherent risks involved in investing.