Note: This entry was written in part as a submission for an ESG Case Competition of which we qualified into the finalists. For the purpose of the blog, I have only included segments I’ve personally written and excluded a portion of the ESG analysis of which I did not contribute.

Cheers,

Thanks for reading Ryan’s Substack! Subscribe for free to receive new posts and support my work.

Ryan

Company Overview

BIM Birelesik Magazalar A.S., a Turkish grocery retailing company established in 1995, operates with a fundamental objective: to offer essential food items and consumer goods to customers of the highest quality at the most affordable prices. This foundational ethos positioned BIM as the trailblazer of the hard-discount model in Turkey. Presently, the company provides an extensive range of approximately 850 items, predominantly comprising premium private label products, thereby pioneering a distinctive retail approach.

Since its inception, BIM has flourished to become the foremost organized grocery retailer in Turkey, commanding a market share estimated at 14% – 16.4% as per consumer surveys and company disclosures. While primarily operating within Turkey, BIM also maintains smaller operations in Morocco and Egypt. Expanding its foothold, BIM entered the hard discount supermarket arena under the FiLe brand in 2015. At present, BIM manages a total of 11,510 stores, with the distribution being 10,370 stores in Turkey, 627 in Morocco, 311 in Egypt, and an additional 202 adopting the File hard discount supermarket format.

BIM's primary target demographic is low-to-middle-income households, thereby strategically situating its stores predominantly within urban locales. In 2021, the company ventured into the realm of e-commerce with the File brand, albeit its contribution to overall sales remains marginal.

Steering the helm is a seasoned and devoted management team, boasting an average tenure of 18.2 years. CEO Mustafa Latif Topbas, equipped with extensive experience in Textile, Industrial, and Commercial sectors, leads the organization. The role of CFO is capably undertaken by Haluk Dortluoglu, a stalwart in international independent audit companies, recognized as "The Best CFO In Turkey." COO Galip Aykac, with over 18 years of executive experience, previously chaired the Board of Directors of the Food Retailers Association from 2019 to 2022. This continuum in senior leadership has been pivotal in enabling BIM to steadfastly execute its strategic vision, navigating shifts in the market and industry landscape.

In terms of Ownership structure, about 47% of BIM is owned by Institutions and Private Corporations. Family ownership accounts for about 26% of the total share outstanding, with the remaining 73% held by public institutions and corporations. The single largest public shareholder includes 1. Vanguard Group at 3%, Blackrock at 2.3% and Norges Bank Investment Management at 1.82%.

Industry Overview

Over the past 15 years, Turkey's organized grocery retailing sector has undergone a noteworthy consolidation, marked by several significant trends and transformations. Primarily, a discernible shift in consumer spending on grocery retailing has been observed, redirecting from traditional outlets often termed as "Mom & Pop" stores, or in Turkey's context, referred to as "Bakkal". According to a survey conducted by the United States Department of Agriculture, these traditional grocery retailers have experienced a gradual annual sales decline of approximately 3% to 5% since 2007, attributable to the ascent of modern grocery establishments.

In the fiscal year 2022, modern grocery stores accounted for around 66% of total grocery retail sales, with the remaining 33% attributed to traditional grocery outlets. Notably, the momentum of this transition remains pronounced, primarily attributed to the modern format's capacity to cater to a broader spectrum of demographics. These patrons are drawn to its heightened hygiene standards, enhanced convenience, superior comfort, and an amalgamation of quality and pricing advantages.

\Another significant development is the ascendancy of "Discount Retailers," emerging as the primary beneficiaries in the transition from traditional to modern retailing. This format, typically characterized by its smaller store footprint, a limited array of Stock Keeping Units (SKUs), and competitive pricing, found its genesis and gained prominence through BIM's pioneering efforts in 1995. Particularly since 2016, the shift in market preference from conventional retailers to discounters, led by entities like BIM, has proven to be profoundly advantageous. During this period, the market share of discount retailers surged from 14% in FY2016 to an impressive 30% by FY2022.

The observed accelerated pace of market share migration from traditional retailers to discounters can be attributed in part to the pronounced levels of food inflation in Turkey. This inflationary environment, fueled by disruptions in the supply chain due to the COVID-19 pandemic and geopolitical tensions like the Ukraine-Russian War, has contributed to this shift. According to data from the Turkish Statistical Institute, food inflation escalated to approximately 60.72% in July 2023, with a zenith of 102.55% in November 2022. These dynamics have provided a structural tailwind for discount retailers, as they naturally align with the preferences of price-sensitive consumers by offering competitively priced groceries and everyday consumer goods.

A noteworthy industry concern revolves around the escalating friction between discount retailers like BIM, A101, SOK, and the Turkish government. The primary contention put forth by the government centers on the assertion that these discount retailers are capitalizing on the prevailing situation, employing unethical price hikes to drive growth at the expense of society. As analysts evaluating both the company and the context, we find this argument lacking in conviction.

Grocery retailers, including major players like BIM, generally operate on thin net margins, typically ranging from 3% to 5%. Even in a scenario where discount retailers were to adopt a margin of 0%, such an adjustment would be overshadowed by the pervasive food inflation rate of 60%. While acknowledging the potential tail risk posed by heightened government scrutiny, our team has proactively engaged with BIM's management to explore and understand the actions and strategies they are implementing to mitigate this specific concern, particularly in relation to reputational risk aspects.

Lastly, a pivotal trend within the grocery retailing industry is the escalating consolidation among its top 5 major participants. In FY2017, these leading players collectively commanded a 21.4% industry share, with BIM as the foremost contributor at 7.5% market share. Fast-forwarding to FY2022, this consolidation surged significantly, with the top 5 players now controlling a substantial 40% market share. Notably, BIM emerged as the principal leader, attaining a noteworthy 17.2% market share.

This pronounced consolidation dynamic within the top 5 players is chiefly attributed to the overarching transition from traditional retailers to their modern counterparts. Additionally, it is influenced by the exit or contraction of smaller participants lacking the requisite economies of scale or operational robustness to contend with the escalating cost pressures.

Business Overview

Operating Philosophy

Similar to other value-driven retailers like Costco, BIM's business model is profoundly consumer-centric. By expanding its customer base, BIM harnesses the power of scale to drive down costs further.

At its core, BIM is underpinned by three fundamental operating principles:

Minimize Extraneous Expenditure: BIM diligently avoids superfluous expenses that could potentially escalate product prices. This encompasses measures such as curtailing excessive advertising and marketing expenditures.

Efficient Quality Oversight: BIM's product portfolio is strategically limited to a stringent selection of 850 items, ensuring a focused and cost-effective approach to maintaining quality standards while providing affordability.

Agile Decision-Making: BIM expedites its decision-making and implementation processes through the establishment of a dynamic logistics and information network connecting regional offices and stores.

Through the embodiment of these three operating principles, BIM crafts a value proposition for consumers characterized by high-quality, dependable, and budget-friendly products.

Hard Discount Model

At the forefront of the "hard discount" model in Turkey, BIM has grown to become a prominent player in the country's retail landscape. This unique approach emphasizes consistently low prices without resorting to discounts or loyalty programs that might create a reliance on price reductions.

Additionally, BIM strategically selects store locations in high-traffic yet less central areas, optimizing footfall while managing rental costs. The stores themselves are notably smaller than traditional supermarkets, reducing rental expenses.

A key element of BIM's strategy is prudent resource allocation, minimizing advertising and marketing expenses to channel savings into lower prices. This approach fosters a cycle of increased foot traffic and larger basket sizes, contributing to economies of scale.

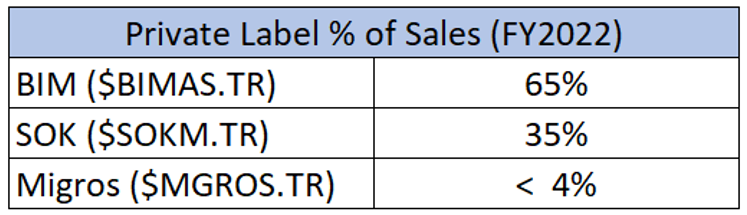

BIM's model also involves curating its product portfolio, limiting it to around 850 Stock Keeping Units (SKUs) with a focus on private labels. This enables BIM to place bulk orders, securing better pricing and shipping efficiencies while maintaining quality control. A significant portion of BIM's sales comes from private label products, making up 65% of total turnover in FY2022 for BIM's own brands, with File sales accounting for 33%. Private label sales are lower for BIM's Morocco and Egypt operations, comprising 24% and 15% of sales, respectively.

Cost Structure

As a retailer, a huge part of expenses goes to purchasing inventories, which accounted for 82% of sales. The remaining costs are spread between marketing expenses (11%) and G&A (1%), of which both personnel expenses accounted for more than 50%. Rental expenses are embedded within marketing and G&A expenses.

Business Moats

BIM's primary strength resides in its value proposition, centered around its capacity to maintain low costs and offer affordable prices—a facet wherein competitors struggle to attain sustainable parity. This ability stems from three foundational pillars:

1. Economies of Scale

BIM's economies of scale find quantitative expression in its operating and net income margins. Notably, BIM's gross margin appears lower in contrast to its peers, largely due to its focus on the low to middle-income customer segment, as opposed to SOKM and Migros, who target a more affluent clientele. Despite this, BIM achieves markedly higher net margins compared to its peers, surpassing them by a substantial 1.5%.

As a market leader, BIM capitalizes on the advantages of bulk purchasing and the ability to spread fixed costs across a broader customer base. Savings accrued from operational efficiency gains through economies of scale are consequently funneled back to customers, manifesting as reduced prices or increased quantities. This practice cultivates customer loyalty, facilitating BIM's expansion of market share, revenue growth, store proliferation, and the establishment of a reinforcing cycle of improvement.

This concept is exemplified in BIM's inventory transportation. The proliferation of BIM stores within a region generates heightened route density for product delivery. This dense network results in significantly reduced shipping costs relative to competitors, as underscored in earnings calls. Moreover, this strategic store density extends an environmental advantage, evident in BIM's notably lower carbon intensity compared to its industry peers.

2. Strong Relationship with Suppliers

While the idea of BIM's robust supplier relationships being a pivotal source of competitive advantage might initially seem less evident, a closer examination brings its significance to the fore—especially when scrutinizing the company's cash conversion cycle in relation to its peers.

At a cursory glance, BIM's negative cash conversion cycle might appear relatively weaker than its competitors. However, comprehending the context within which this negative cycle operates is essential. BIM exhibits the shortest inventory days among its peers, coupled with higher accounts receivable days and briefer account payable days. This interplay stems from two core factors.

Firstly, the shorter account payable days are likely attributed to BIM's adeptness in capitalizing on early payment discounts extended by vendors. While not explicitly stated, this practice of vendors incentivizing prompt payment is not uncommon. Notably, Atradius' 2019 market research on payment practices in Turkey reveals that a higher percentage of respondents in Turkey (26%) offer discounts for timely invoice settlement compared to Eastern Europe (18%). Given BIM's keen focus on optimizing cost-saving initiatives, this approach aligns with its strategy.

Secondly, the more lenient accounts receivable collection terms contribute to maintaining operational liquidity for suppliers, especially within challenging macroeconomic contexts. This measure safeguards supplier viability, mitigating churn and thus ensuring the quality of private label offerings—particularly significant given the substantial proportion of private label products within BIM's overall turnover.

These strategic approaches collectively underscore the significance of BIM's strong supplier relationships, reflecting a nuanced and contextually guided competitive advantage.

3. High Consumer Trust in Private Labels.

We firmly hold the perspective that BIM's distinctively elevated levels of private label sales, when contrasted with those of its competitors, establish a lasting competitive advantage for the company vis-à-vis its peers. Throughout FY2022, BIM's private label sales contributed a substantial 65% to its total sales—an impressive figure that nearly doubles that of its closest competitor.

Insights from İlayda Saraçoğlu, a marketing analyst from Bahçeşehir University in Turkey, offer valuable context in understanding the challenges faced by companies like Migros in elevating their private label market share to levels akin to their core geographic operations. This challenge emerges due to Turkish consumers' inherent reliance on national brands. Consumers often discern quality disparities between these private labels and dominant national brands, thereby necessitating efforts to dispel concerns over perceived quality differences. Notably, BIM has adeptly addressed this concern since its inception in 1995, consistently employing marketing endeavors to underscore the high-quality attributes of its private label offerings.

Considering the more favorable economics underpinning private label products compared to third-party brands, BIM's higher relative penetration of private labels not only bolsters its value proposition but also effectively leverages the associated higher margins. This dynamic furnishes BIM with a strategic advantage that outpaces its peers.

Key Thesis: Secular Growth driven by TAM expansion and Market Share Gains

In FY2022, there was a notable 92.5% increase in revenue growth for like-for-like sales, partly attributed to the pronounced food inflation of 85.5%. Notably, we perceive the prevalent inflationary environment in Turkey as a favorable factor for BIM, propelling both enhanced Total Addressable Market (TAM) expansion and augmenting market share gains.

BIM's positioning as a discount retailer positions it as a refuge for consumers amidst economic pressures, owing to its affordability in consumer goods. Simultaneously, BIM's robust cost structure vis-à-vis its competitors equips it to manage inflation-induced cost pressures, effectively transmitting minimal price hikes to consumers, thereby maintaining sustainability.

As of FY2022, BIM's market share stands at approximately 15% - 17%, sourced from company data and consumer surveys. Grounded in our projections, this trajectory of escalating market share is anticipated to continue at an accelerated pace, primarily drawing from smaller organized retailers and traditional retailers categorized as "others." Moreover, within the top 5 retailers' market share in Turkey, its current representation at 40%, up from 20% in FY2017, indicates room for further industry consolidation. This elevation in BIM's market share is fueled by two pivotal factors: 1) Amplified organic foot traffic and expenditure within existing BIM stores due to structurally increases in traffic for discount retailers and 2) BIM's penetration into the supermarket segment through its "File" stores. As of FY2022, File stores have reached a count of 202 and are poised for further expansion in FY2023. Remarkably, File branded supermarkets have already secured 0.5% of Turkey's grocery retail consumption, a substantial rise from 0% in FY2019. Our optimism in the File format's potential to secure the second-largest market share segment within store types is anchored in the identical competitive advantage that distinguishes BIM from its competitors.

Lastly, a structural TAM expansion underscores BIM's growth trajectory. The supermarket segment's inclusion contributes to TAM expansion, but the predominant factor remains the sustained shift of spending from traditional grocery retailers to modern counterparts. Historical trends indicate a gradual 3% market share loss on average among traditional grocery retailers, largely benefiting discount retailers. Presently, modern retailers command a 66% market penetration. We anticipate the eventual equilibrium between modern and traditional retailers to settle around an 80/20% split, akin to more advanced economies such as Singapore, Japan, and Korea—a perspective corroborated by a McKinsey report on Southeast Asia's grocery landscape.

We are confident that this enduring trend will continue, imparting a substantial tailwind to BIM's capacity to leverage its economies of scale and deliver high-quality products at unparalleled prices, a capability that eludes its competitors.

Supplemental Thesis: Further Expansion in EBIT Margins Driven by File Format Profitability and Private Label Penetration

The team firmly believes that the central thesis will exert a robust, near-term, and substantive impact on the business. However, our assessment also identifies a longer-term prospect that we consider BIM is aptly positioned to capitalize on. In FY2015, BIM ventured into the supermarket segment through its innovative "File" format, which currently commands a 33% market share by store type. This new format entails stores spanning around 1000 square meters—roughly 2-3 times larger than typical store sizes—and housing approximately 3,500 SKUs, significantly more than the standard 850-product portfolio.

Presently, there exist 202 File stores, primarily operating within Turkey. BIM's strategic intent to double its footprint within this segment signals a commitment to expanding its influence and seizing market share from established players like Carrefour and Migros. We are confident that BIM, armed with the competitive advantages delineated earlier, is poised for successful execution vis-à-vis its peers. Looking into the longer horizon, we envision two primary benefits stemming from the escalating sales emanating from File format stores:

1. Enhancement of Overall Gross Margins through Improved Customer Mix:

When juxtaposed with key competitors in Turkey, BIM exhibits a notably lower gross margin—a reflection of its targeted approach towards the lowest income segments. Anticipating an upsurge in sales originating from File formats, we anticipate a concurrent elevation in gross margin owing to the influence of a more favorable customer mix.

2. Augmentation of Overall Profitability via the Maturation of File Stores and Amplified Private Label Penetration:

Note: Error on the right chart. I meant “[BIM]/[File] Sales Breakdown by Product Type”

BIM's File stores have reached a pivotal point in profitability, experiencing an accelerated trajectory due to economies of scale. A comparatively higher proportion of third-party labels within BIM's File stores, coupled with a broader product portfolio, has historically exerted a dampening effect on overall profitability. However, noteworthy strides have been made—FY2019/FY2020 witnessed positive EBITDA margins and net profitability for BIM's File stores. Moreover, the current relatively lower penetration of private label offerings within File stores presents an avenue for further enhancement, promising a favorable impact on overall margins.

In conclusion, we firmly contend that BIM's calculated expansion in the File format not only aligns with the present momentum but also positions the company strategically to extract sustainable benefits, both in terms of enhanced profitability and amplified market presence.

Risk and Mitigations

The team believe that there are 2 material areas of risks that would require deeper consideration of the impact on the company’s performance. Firstly, we believe the potential regulatory intervention or policies could be a structural headwind for BIM given the current level of tensions between discount retailers and the government. Secondly, we believe that the competition as well as the overall macroeconomic environment may result in BIM unable to achieve its desired goals.

1. Regulatory Conflicts and Unfavorable Policies

In October 2021, discount retailers, including BIM, SOK, Migros, and CarrefourSA, incurred fines totaling $2.7 billion Turkish lira (equivalent to $283 million) for contravening antitrust regulations. The principal allegation asserts that these retailers are the underlying catalysts behind escalating prices and inflation within the country. It is posited that these entities have implemented exploitative pricing strategies to capitalize on the prevailing circumstances. BIM, in particular, was penalized with 958.1 million Turkish lira, approximating nearly 10% of its net income.

Of particular concern to our team is the potential impact on reputational risk. In December 2022, Turkish newspapers reported a backlash against the country's discount retailers following assertions by the Turkish President. These statements accused retailers of exacerbating inflation through steep price hikes and alleged affiliations with terrorism.

Predicated on our conducted due diligence and collated data, we observed a decline in the top 5 market share percentages during FY2022 as compared to FY2011. This shift partly redirected market share from modern retailers to traditional counterparts—an initiative initiated by the Turkish government to bypass intermediaries.

It is our conviction that if such conflicts persist, they could potentially precipitate significant and enduring reputational risks for BIM and other contemporary grocery retailers. To preclude such outcomes, we have noted the strategic measures being undertaken by the company. Notably, BIM is intensifying its corporate communications efforts to elucidate its role and demonstrate that it functions as a counter-inflationary entity owing to its economies of scale, enabling lower pricing. The management has also conveyed that BIM lacks the capacity to influence currency strength and import costs of goods. Even if BIM were to operate at a 0% profit margin, its impact on the rampant 60-80% inflation would remain marginal.

We hold the perspective that BIM's emphasis on augmented corporate communication initiatives and a resolute stance against these allegations is prudent. Further, we perceive industry-wide collaboration as an additional mechanism to mitigate such risks.

Conclusion

In conclusion, BIM stands as a fundamentally resilient and high-caliber enterprise, strategically positioned to harness substantial advantageous trends and aligned with sustainability strategy. BIM's operational ethos of upholding cost efficiency while extending these benefits to its clientele holds particular significance in our evaluation, as it constitutes a pivotal contribution to Turkish society during these intricate times. Our assessment underscores the strategic advantages that underscore BIM's trajectory—chief among them, a cost-effective framework driven by economies of scale, the notable trust customers vest in its private labels, and the robustness of its supplier affiliations. These combined strengths position the company favorably to seize synergistic opportunities. As BIM broadens its Total Addressable Market (TAM), heightens profitability, and strengthens its market presence, these dynamics are poised to be instrumental in its sustained triumph. Additionally, we hold the view that BIM's present valuation offers a substantial margin of safety. It is our conviction that BIM is strategically poised to navigate and leverage the current macroenvironment to its advantage.

Thanks for reading Ryan’s Substack! Subscribe for free to receive new posts and support my work.